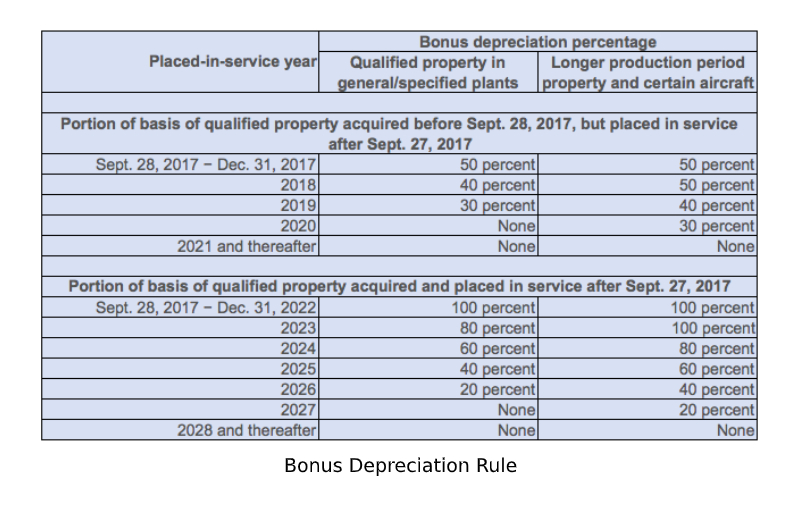

Also following 2017 Tax Reform, the cost of qualifying property of no more than $500,000 per piece can be deducted for tax purpose. In addition, additional first-year depreciation deduction is allowed equal to 50% of the adjusted basis of qualified property. Qualifying property is also extended to property already put in service. The ability to depreciate assets upfront provides strong incentive for fixed asset investment.

{kind=link}

{kind=link}

{kind=link}

{kind=link}